Send us a message

We would like to learn more about your challenges and to understand how we can support you.

Get in touch.

Send us a message and we’ll get

back to you within 48 hours.

Alternatively, email

hello@shiifttraining.com

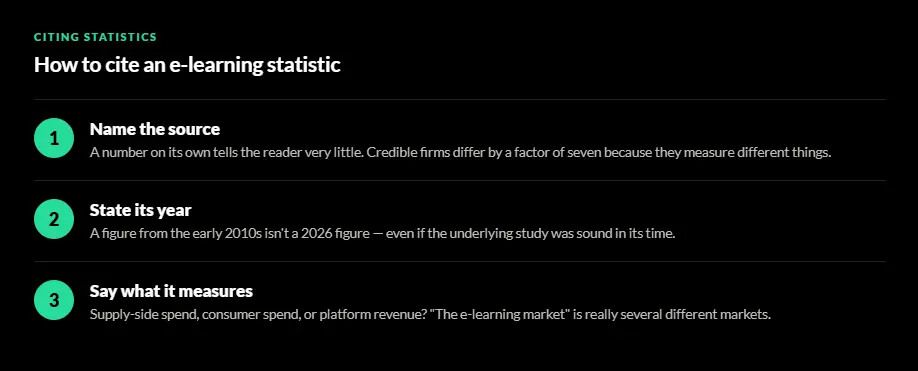

Search for e-learning statistics and you’ll find the same handful of figures repeated across hundreds of pages, often without a source you can actually check. Some of those numbers are sound. Others have been copied so many times that nobody seems to know where they started. This piece sticks to figures that trace back to a named, datable source, and it flags the popular stats that don’t.

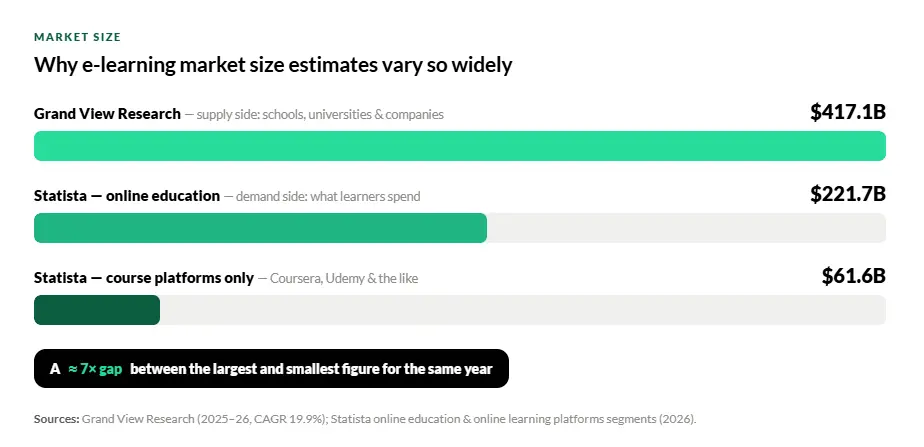

The first thing worth understanding is that there isn’t one e-learning market, so there isn’t one market size. Research firms count different things. One measures the money companies and schools spend on learning services. Another measures what individual consumers pay for online courses. They use different methods and they land far apart, which is why you’ll see “the e-learning market” valued anywhere from about $60 billion to well over $400 billion for the same year. Both can be correct. They’re answering different questions.

On the supply side, Grand View Research valued the global e-learning services market at $353.0 billion in 2025 and expects it to reach $417.1 billion in 2026, growing at a compound annual rate of 19.9% to roughly $1,485 billion by 2033. That estimate covers spending by schools, universities, and companies on services such as course development and learning platforms.

On the demand side, Statista puts the global online education market at about $221.7 billion in 2026, growing at 6.86% a year to around $289 billion by 2030. Statista’s figure mostly reflects what individual learners spend across university programs, course platforms, and professional certificates. Narrow that further to standalone course platforms like Coursera or Udemy, and Statista’s online learning platforms segment comes to just $61.6 billion in 2026.

So a sevenfold gap separates the largest and smallest “e-learning market” figures for the same year, and the gap is about definitions. When you cite a market size, name the firm and say what it’s measuring. A number on its own tells the reader very little.

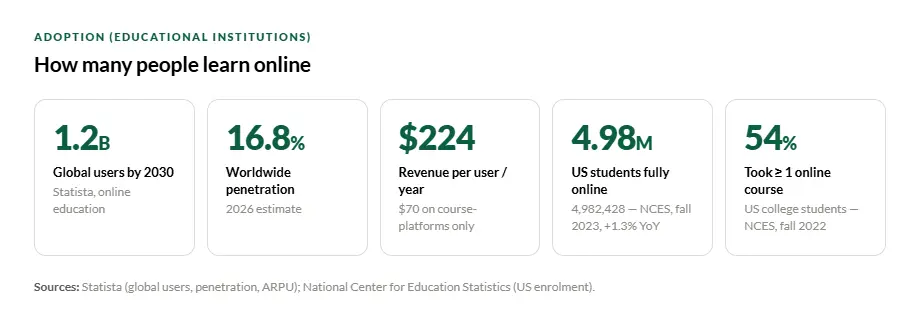

Statista estimates the global online education market will pass 1.2 billion users by 2030, with worldwide penetration around 16.8% in 2026. Average revenue per user sits at about $224 a year on its broad measure, though that drops to roughly $70 on the narrower course-platforms segment. That gap is a useful reminder that most online learning revenue comes from accredited university programs rather than the consumer apps people tend to picture, since the university segment alone accounts for about $152 billion of the 2026 total.

For hard adoption data rather than spending estimates, US higher education offers some of the most reliable figures, because American institutions report their enrollment to the federal government every year. According to the National Center for Education Statistics, just under 5 million US students (4,982,428) were enrolled exclusively in distance education in fall 2023, up 1.3% on the year before. Counting everyone who took at least one online course, that share reached 54% of US college students in fall 2022, according to NCES data.

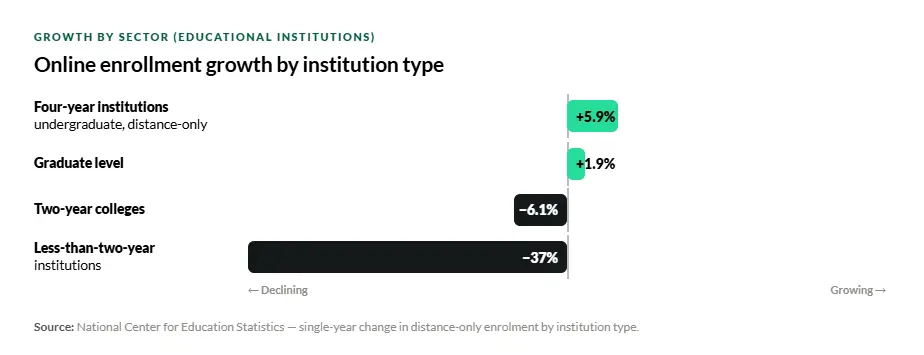

The headline that “online learning keeps growing” hides a more interesting split. NCES found that fully online enrollment rose at four-year institutions, where undergraduate distance-only enrollment grew 5.9% in a single year, and it rose at the graduate level too, up 1.9%. Over the same period it fell at two-year colleges by 6.1% and dropped by 37% at less-than-two-year institutions. Online study is consolidating around degree-granting universities and graduate programs while shrinking in shorter vocational settings. Anyone quoting a single “online enrollment is up” figure is flattening a picture that moves in opposite directions depending on the type of institution.

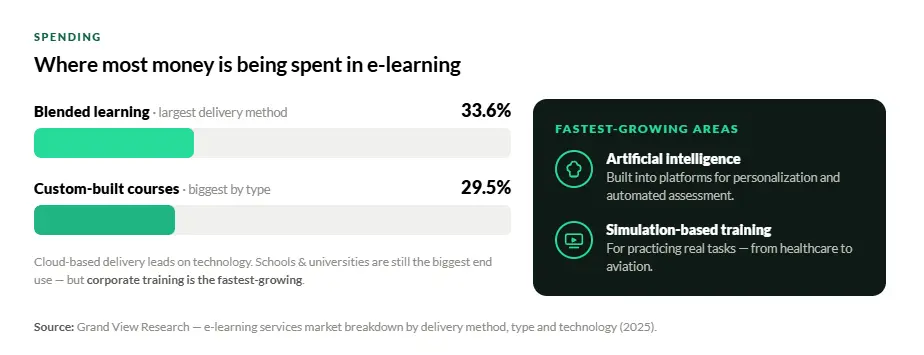

Grand View Research’s breakdown of the services market shows blended learning, which mixes live instruction with digital content, as the largest single delivery method at 33.6% of the market in 2025. Custom-built courses make up the biggest share by type at 29.5%, and cloud-based delivery leads on technology. Schools and universities still account for the largest slice of spending, but corporate training is the fastest-growing end use, as companies move workforce training and compliance online.

Two technology areas are growing faster than the rest, according to the same report. The first is artificial intelligence, which is being built into platforms for personalization and automated assessment. The second is simulation-based training, used where people need to practice real tasks in fields that run from healthcare to aviation. If there’s a single theme in the corporate e-learning statistics for 2026, it’s that money is shifting toward content that adapts to the learner and toward formats that let people rehearse rather than just watch.

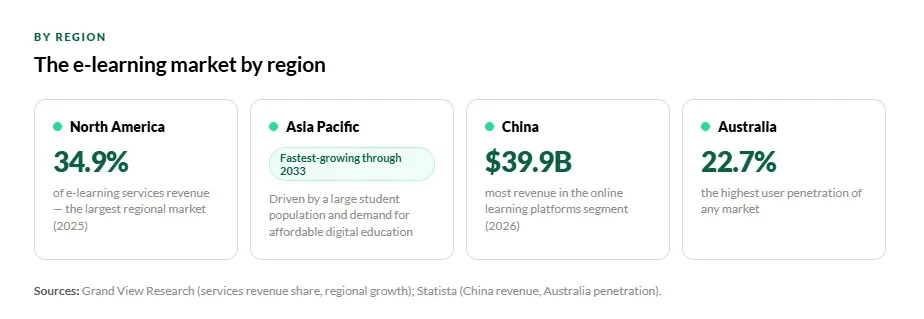

North America remained the largest regional market in 2025 at 34.9% of e-learning services revenue, according to Grand View Research, helped by mature infrastructure and a concentration of established providers. Asia Pacific is forecast to grow fastest through 2033, driven by a large student population and demand for affordable digital education. Statista’s consumer figures tell a similar story from a different angle. China generates the most revenue in the online learning platforms segment, around $39.9 billion in 2026, while Australia has the highest user penetration at about 22.7%.

Several of the most-shared e-learning statistics don’t hold up when you try to trace them. We’ve left them out of the figures above, and here’s why.

One involves corporate savings: that IBM saved $200 million by moving training online, that Dow Chemical cut per-learner costs from $95 to $11, or that companies with e-learning see “218% higher revenue per employee.” These trace back to reports from well over a decade ago and then get presented as if they describe today’s market. The underlying studies may have been sound in their time, but a figure from the early 2010s isn’t a 2026 figure.

Then there’s the line that online learning has grown “900% since 2000.” It’s repeated constantly with no consistent source and no clear definition of what’s being counted. Without those, it works as a slogan and not as evidence.

Finally, treat any single “the e-learning market is worth $X” claim with suspicion unless it names the firm and the definition. As the market-size section showed, credible sources differ by a factor of seven because they’re measuring different things.

What the numbers actually say

Deliver next generation training. Get in touch.

Email us at hello@shiifttraining.com or send

us a message and we’ll be in touch within 48hrs.